What the Frack? a short term, toxic bubble

- fracking is the future?

- Art Berman

- Dave Cohen

- James Kunstler

- ASPO USA: Panacea or Chimera?

- 2012: Energy Dept lowers estimate of Marcellius gas

- fracking is a toxic, desperate effort to maintain natural gas and petroleum supplies. Conventional oil peaked in the USA in 1970 and conventional natural gas peaked in 1973. Fracking has not raised domestic oil production above this level, although the conventional natural gas peak has been surpassed, temporarily.

- fracking cannot provide "100 years" of natural gas for the US, even if environmental and public health concerns are ignored. Fracked wells deplete faster than conventional wells and take more technical expertise, money and energy to drill.

- the consequence for banning fracking would be an immediate reduction or end of burning natural gas for electricity and the start of gasoline rationing. This is why environmental objections to fracking have not been successful.

US Department of Energy estimates that "conventional" natural gas will sharply decline in the 2010s and shale gas (from "fracking") will supposedly increase to keep gas supplies high. But many fracked gas wells deplete rapidly and are unlikely to meet the "irrational exuberant" expectations that many have for this technology. key links about shale gas hype: petroleumtruthreport.blogspot.com www.shalebubble.org www.postcarbon.org/report/331901-will-natural-gas-fuel-america-in |

|

www.guardian.co.uk/environment/earth-insight/2013/jun/21/shale-gas-peak-oil-economic-crisis

Shale gas won't stop peak oil, but could create an economic crisis

overinflated industry claims could pull the rug out from optimistic growth forecasts within just five years

by Nafeez Ahmed, June 21, 2013

www.aspousa.org/index.php/2010/07/interview-with-art-berman-part-1/

Interview with Art Berman - Part 1

By Arthur Berman • on July 19, 2010

Art Berman is a geological consultant whose specialties are subsurface petroleum geology, seismic interpretation, and database design and management. He is currently consulting with a wide range of industry clients such as PetroChina, Total, and Schlumberger. Mr. Berman has an MS in geology from the Colorado School of Mines and is active with the American Assoc. of Petroleum Geologists. Art spoke with us last Thursday after a presentation in Canada at the CIBC Technical Conference.

POR: Can you give us your latest updated perspective on the shale gas story?Art Berman is a geological consultant whose specialties are subsurface petroleum geology, seismic interpretation, and database design and management. He is currently consulting with a wide range of industry clients such as PetroChina, Total, and Schlumberger. Mr. Berman has an MS in geology from the Colorado School of Mines and is active with the American Assoc. of Petroleum Geologists. Art spoke with us last Thursday after a presentation in Canada at the CIBC Technical Conference.

Art Berman: You have to acknowledge that shale gas is a relatively new and significant contribution to North American supply. But I don’t believe it’s anywhere near the magnitude that is commonly discussed and cited in the press. There are a couple of key points here. First the reserves have been substantially overstated. In fact I think the resource number has been overstated.

If you investigate the origin of this supposed 100-year supply of natural gas…where does this come from? If you go back to the Potential Gas Committee’s [PGC] report, which is where I believe it comes from, and if you look at the magnitude of the technically recoverable resource they describe and you divide it by annual US consumption, you come up with 90 years, not 100. Some would say that’s splitting hairs, yet 10% is 10%. But if you go on and you actually read the report, they say that the probable number-I think they call it the P-2 number-is closer to 450 Tcf as opposed to roughly 1800 Tcf. What they’re saying is that if you pin this thing down where there have actually been some wells drilled that have actually produced some gas, the technically recoverable resource is closer to 450. And if you divide that by three, which is the component that is shale gas, you get about 150 Tcf and that’s about 7 year’s worth of US supply from shale. I happen to think that that’s a pretty darn realistic estimate. And remember that that’s a resource number, not a reserve number; it has nothing to do with commercial extractability. So the gross resource from shale is probably about 7 years worth of supply.

For a project that a colleague and I did for a client, I actually went in and looked at all the shale plays and assigned some kind of a resource number to them. I also used some work that was done by Wendell Medlock at Rice University’s Baker Institute. He did an absolutely brilliant job of independently determining what the size of the resource plays in Canada and the US might be.

The resource hasn’t been misrepresented but the probable component has not been properly explained as a much smaller component of the total resource; I guess they just didn’t read the PGC’s report carefully enough. If you take the proved reserves plus the report’s probable technically recoverable number, we have something like 25 years of natural gas supply in North America, which is quite a bit. It’s a lot. I don’t say any of this to give shale gas a bad name.

The other interesting thing about the PGC’s report that nobody seems to pay attention is this: they said there is something like 650 Tcf of potential shale gas. Well, there’s 1000 Tcf of something else. What’s the something else? It’s conventional reservoirs plus non-shale/non-coalbed-methane unconventional reservoirs. So there’s 70 percent more resource in better quality rocks than shale. It just astonishes me that nobody has paid any attention to that.

So that’s the simple view. And then the other thing that we see empirically is that if you look at any of these individual shale-gas plays-whether it’s the Haynesville or the Barnett or the Fayetteville-they all contract to a core area that has the potential to be commercial that is on the order of 10 to 20 percent of the geographic area that was originally represented as all being the same. So if you take the resource size that’s advertized-say for the Haynesville shale, something like 250 Tcf-and you look at the area that’s emerging as the core area, it’s less than 10 percent of the total. So is 25 Tcf a reasonable number for the Haynesville shale? Yeah, it probably is. And it’s a huge number. But the number sure is not 250 Tcf, and that’s the way all of these plays seem to be going. They remain significant. It hasn’t been proved to me yet that any of it is commercial, but they’re drilling it like mad, there’s no doubt about it.

Those are sort of the basic conclusions. And when you look at it probabilistically, which I think is the only intelligent way to look at anything which you have any uncertainty about, what you realize is that the numbers that are being represented by all of these companies as “truth” are probably like the P-5 case, having a 5 percent probability of being true. So they say, “well, our average well in the Haynesville is going to be 7 Bcf,” and I say there will certainly will be wells that make 7 Bcf but there’s no way that the average is that high. My take is that there will probably be 5 percent of wells that will make 7 Bcf.

I just think everybody is caught up in this. I have a slide where I say, you guys need to get over the love affair and get on with the relationship. You keep talking about how big it is and how great it is, but at some point you have to live together and that’s hard work. You have to be honest with yourself and with each other and you have to do some work. I just don’t think we’ve moved past the love affair.

One other important thing is the Barnett shale. We keep coming back to it because it’s the only play that has much more than 24 months worth of history. I recently grouped all the Barnett wells by their year of first production. Then I asked, of all the wells that were drilled in each one of those years, how many of them are already at or below their economic limit? It was a stunning exercise because what it showed is that 25-35% of wells drilled during 2004-2006-wells drilled during the early rush and that are on average 5 years old-are already sub-commercial. So if you take the position that we’re going to get all these great reserves because these wells are going to last 40-plus years, then you need to explain why one-third of wells drilled 4 and 5 and 6 years ago are already dead.

POR: When you say one-third of the wells are already sub-commercial, do you mean they have been shut in, or that they are part of a large pool where no one has sharpened the pencil?

Berman: Some of them never produced to begin with. No one talks about dry holes in shale plays, but there are bona fide dry holes-maybe 5 or 6 or 7 percent that are operational failures for some reason. So that’s included. There are wells that, let’s just call them inactive; they produced, and now they’re inactive, which means they are no longer producing to sales. They are effectively either shut-in or plugged. Combined, that’s probably less than 10 percent of the total wells. But then there are all the wells that are producing a preposterously low amount of gas; my cut-off is 1 million cubic feet a month, which is only 30,000 cubic feet per day. Yet those volumes, at today’s gas prices, don’t even cover your lease/operating expenses. I say that from personal experience. I work in a little tiny company that has nowhere near the overhead of Chesapeake Energy or a Devon Energy. I do all the geology and all the geophysics and there’s four or five other people, and if we’ve got a well that’s making a million a month, we’re going to plug it because we’re losing money; it’s costing us more to run it than we’re getting in revenue.

So why do they keep producing these things? Well, that’s part of the whole syndrome. It’s all about production numbers. They call these things asset plays or resource plays; that reflects where many are coming from, because they’re not profit plays. The interest is more in how big are the reserves, how much are we growing production, and that’s what the market rewards. If you’re growing production, that’s good-the market likes that. The fact that you’re growing production and creating a monstrous surplus that’s causing the price of gas to go through the floor, which makes everybody effectively lose money….apparently the market doesn’t care about that. So that’s the goal: to show that they have this huge level of production, and that production is growing.

But are you making any money? The answer to that is…no. Most of these companies are operating at 200 to 300 to 400 percent of cash flow; capital expenditures are significantly higher than their cash flows. So they’re not making money. Why the market supports those kinds of activities…we can have all sorts of philosophical discussions about it but we know that’s the way it works sometimes. And if you look at the shareholder value in some of these companies, there is either very little, none, or negative. If you take the companies’ asset values and you subtract their huge debts, many companies have negative shareholder value. So that’s the bottom line on my story. I’m not wishing that shale plays go away, I’m not against them, I’m not disputing their importance. I’m just saying that they haven’t demonstrated any sustainable value yet.

Commentary: Interview with Art Berman—Part 2

By the Peak Oil Review team

(Note: Commentaries do not necessarily represent the ASPO-USA position.)

Art Berman is a geological consultant whose specialties are subsurface petroleum geology, seismic interpretation, and database design and management. He is currently consulting with a wide range of industry clients such as PetroChina, Total, and Schlumberger. Mr. Berman has an MS in geology from the Colorado School of Mines and is active with the American Assoc. of Petroleum Geologists. He spoke with us about 10 days ago, after a presentation in Canada at the CIBC Technical Conference. (Part 1 appeared last week, in the July 19th issue of the POR.)

POR: How have analysts and investors responded to your studies and your viewpoints?

Berman: My biggest clients, for this kind of talk and work, are investment bankers and investment advisory companies. I gave two talks in Calgary over the last week—one to CIBC and the other to Middlefield Capital. I’ve given multiple talks to energy investment companies. They’re the peoplewho are really paying attention to this. The answer is that a significant portion of the investment banking sector takes what I’m saying quite seriously, but what they do with that I can’t tell you.

POR: How has the gas-producing industry responded to your studies and views?

Berman: The U.S. companies have pretty much chosen to ignore me. Or they’ve made public statements that I’m a kook or I don’t understand or I’m hopelessly wrong. Some them—especially the Canadian companies for some reason—want me to advise them even though my message is not a message that they prefer.

It’s a fascinating process. My sense of it is that the level of interest, and whatever notoriety I have, has only increased. I credit the ASPO 2009 peak oil conference in Denver with really kicking that off. That presentation was a tipping point in awareness about the truth of shale gas reserves and economics. After my presentation, I had almost five hours of discussions with analysts that had attended the talk. Associated Press reporter Judith Kohler published an article ― Analyst: Gas shale may be next bubble to burst that was distributed to hundreds of outlets in the national press and that brought this topic into the mainstream. U.S. E&P executives responded with a series of ad hominem opinion editorials and earnings meeting statements that minimized the fact-based positions that were presented at the ASPO 2009 meeting.

Before that, I spent months making presentations to professional societies of geologists, geophysicists and engineers throughout the Gulf Coast. These are colleagues who do the work of the petroleum industry that gave me what amounted to a peer review. I know that there were silent people in those audiences who disagreed with me, but the overall response was supportive and enthusiastic. I also got hundreds of e-mails responding to my World Oil articles that included testimonials about companies' experience with shale gas wells in the real world.

E&P executives don't have any such base, nor do they know about this experience. In all of my presentations, I acknowledge people that include some of the most respected E&P CEOs, opinion leaders, and experts on oil and gas price formation, reservoir engineering, economic evaluation and risk analysis. In addition, there are also many industry analysts in research companies, financial advisory and fund management firms, and reporters in the energy press that consult and publish opinions about my position on shale gas.

The point is that I am not alone. I have a large community of supporters with impeccable credentials. I am a cautious and somewhat conservative person in my professional work because I advise clients on high-risk and very large bets on wells and investments. My reputation and future income depends on the credibility of my evaluations and the quality of my research. I do not believe that the same can be said for the CEOs of the U.S. public companies that dispute my findings.

I’m a fairly busy guy, and a lot of people want to hear the story; I talk to Bloomberg and Platts and others all the time. If anything, I feel as if I’m sort of slipping into the mainstream, in a weird way. It’s a scary thought. I’m now asked to participate in august panel discussions, albeit representing the radical fringe; but a year ago nobody even wanted to talk to me.

I don’t know where it’s going. It seems inevitable to me that it is sort of a bubble phenomenon; but bubbles can go on for 25 years or so, even though everyone knows that’s what’s happening. As long a capital markets continue to fund these things it’s going to keep on going. I’m not saying that’s even a bad thing, though I wouldn’t put any money in it, that’s for darned sure.

POR: Back in the 1960’s the phrase “too cheap to meter” was introduced, by some promoters, as being the future of nuclear energy. Over time, the reality obviously didn’t match the hype. It feels to us that there could be a parallel with the recent 100-year-supply statement...

Art Berman: It could be a big denial issue....

POR: Like that early era for atomic power, the shale gas story still seems so new that there are a lot of uncertainties about the shale gas bucking bronco, if you will. How will the industry respond to the uncertainties? How are they responding to the current tough price signals?

Berman: Not at all right now. I had a whole series of talks that I gave last spring called, ―North American Natural Gas: Acknowledging the Uncertainty.‖ That’s all I want people to do. Not that they shouldn’t drill for it or that I’m right; all I’m saying is acknowledge the uncertainty.

POR: How do you think the Macondo well fiasco will impact US gas and oil production? We’re particularly thinking in the mid- to long-term scenarios.

Berman: Just what’s happened already has had a pretty negative effect on the US economy. The moratorium has caused some rigs to move to other countries. So it seems to me that the inevitable outcome, at some point, is that we’ll have even more dependence on imported crude oil. I just don’t see any other way around it. The intangible piece of that really is how it will affect the planning of companies that want to continue exploring in the Gulf of Mexico. Do they immediately de- emphasize all of that because we just don’t know what the government is going to do to them? And I think the answer to that, despite what they say, is ―yah, sure.

The deepwater Gulf of Mexico is really it. That’s the only substantial source of new reserves of crude oil that the United States has. For now, the whole area has a big question mark on it.

POR: How about the impact on offshore oil and gas production elsewhere in the world? There is already talk of modifying standards and rules in some other offshore basins.

Berman: That’s another unknown. It can’t be good for the energy industry. There are some countries that’s couldn’t care less; they’re just happy to have the rigs come into their waters. But there are certainly countries—like Canada and the UK and Norway—that will certainly put more regulations on it. It will likely have the net effect of slowing offshore operations down and making things cost more. I’m not here to say that that’s wrong.

I personally think the current administration is milking this thing for all the political capital they can. Nobody who’s handling this for them really knows much about the oil and gas business. You have a theoretical physicist running the Department of Energy and I’m sure he’s a very intelligent and high- integrity guy but he didn’t really know anything about drilling or petroleum and I don’t think Salazar is particularly schooled in it. President Obama doesn’t know anything about it. So you have a bunch of amateurs dealing with something that needs a bunch of professionals. Even on the networks and cable news shows, I haven’t seen anybody they’ve brought on who knows anything about it. A lot of interesting people get in front of the cameras and talk: college professors and oceanographers and image analysis specialists and the director of a center for biodiversity—he seems like a real smart guy—but they don’t know anything about drilling operations or petroleum. I don’t say that hyper- critically; it’s just a fact.

POR: Switching over to oil...A number of oil industry CEOs—Christophe de Margerie, James Mulva, etc.—have said world oil production is likely to top out in the 90-95 million barrels/day level, probably during this decade. Where do you see world oil production going in the future?

Berman: That’s not an area where I’ve done a lot of current research. I’m really just answering from the standpoint of what I’ve read others say. I agree with the comments of the CEOs that you named. It just seems like such a stretch to me that we could ever get to the kinds of levels of production that some groups like CERA [Cambridge Energy Research Associates] say we can. It just makes huge sense to me that the big oil exporting countries will continue using more and more of their own petroleum for their own internal uses. How does anybody think that they are going to actually increase the amount of exported oil to get to 95 million or 100 million barrels a day or whatever the forecast number is? From what I read, it looks like the odds are stacked against getting production much higher than it is right now. And we’re in kind of a good place now because demand is way down. US demand has been down nearly 2 million barrels a day below what it was in 2008; that’s huge. How long will that last? We don’t know, but assuming we’re in a recovery— and it kind of looks that way from a natural gas consumption perspective—if and when oil demand ramps up I think we’re going to know the answer very quickly. And the answer’s going to be, we’ll struggle to maintain...that’s my belief.

www.declineoftheempire.com/2010/03/betting-the-house-on-shale-gas.html

03/28/2010

Betting The House On Shale Gas

This is the first of a two stories on shale gas. Today I will put the Shale Gas Boom in proper context. Tomorrow I will explain why I think there is a bubble in shale gas production.

Penn State professor Frank Clemente, testifying before a Senate hearing on natural gas in October, 2009, had this to say—

Natural gas price in the next decade is one of the most important U.S. energy questions. Steadily increasing U.S. dependence on gas poses risk to higher energy prices and electric reliability and national energy security, especially because the Energy Information Administration (EIA) projects natural gas supply to decline 4 percent through 2020...

Where Will We Get the Gas?

Despite our starkly negative experiences with higher natural gas prices and the debilitating volatility of those prices, optimism for the fuel appears to be a contagion.

Several groups have suggested that natural gas can be substituted for coal as the primary fuel for generating electricity. Others have proposed that natural gas can provide fuel for vehicles, and yet even others have argued that we can continue to build wind turbines at a frenetic rate because natural gas will be there to back up this highly intermittent supply.

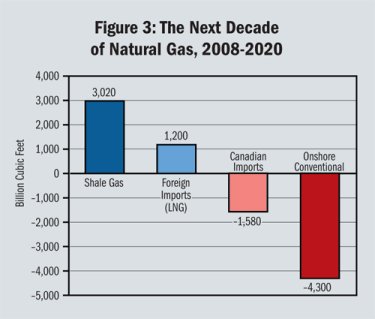

When one objectively examines the data, however, these questions are moot. The real question is: Can natural gas production even meet existing demand, let alone incremental demand? As Figure 3 shows [below], the EIA has projected that by 2020 conventional onshore natural gas production in the U.S. will decrease more than 34 percent, and supplies from Canada will drop 60 percent.

These declines will be only partially offset by two highly questionable new sources: shale gas and liquefied natural gas (LNG) imports. It is important to consider the limitations and unknowns of each in turn.

And you thought I was a pessimist! However, here Frank relies on an EIA forecast, and such forecasts are notorious for containing mountains of bullshit. The EIA's preliminary 2010 Annual Energy Outlook (AEO) is a case in point. Nonetheless, I will quote it below. Clemente's Figure 3 shows that we will get a little over 3 trillion cubic feet (Tcf) of gas from shales in 2020, but another excellent report puts the number at 4.5 Tcf. Both numbers come from the EIA! No doubt the two analysts are using EIA outlooks from different years.

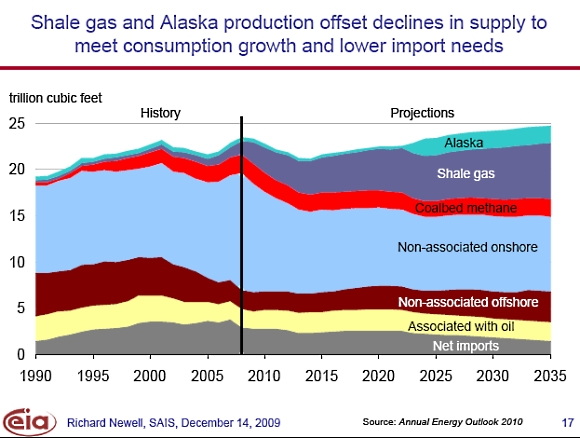

Here's the EIA's 2010 gas outlook—

[posted above]

You can clearly see that natural gas production is lower than it's historical peak (black line) in 2020. That's not good. And you can also see that the shale gas share must get bigger & bigger for us to achieve this unhappy outcome. Let's get back to Frank—

Shale gas production. This is the only bright spot in the domestic supply picture, and substantial reserves exist. There are questions, however, along four key lines:

• Deliverability at scale. Although the shale gas resource is extensive, even the relatively optimistic EIA projections indicate increases in shale gas will offset only about half of supply declines in other key sources (e.g., Canada). Decline rates in shale gas wells can approach 70 percent the first year, creating a constant treadmill to find additional resources and drill new wells.

• Environmental and water impact. The impact of the fracturing process is a matter of growing concern, particularly in New York and Pennsylvania regarding the Marcellus shale play. The Congressional Research Service, for example, recently reported, “The hydraulic fracturing treatments used to stimulate gas production from shale have stirred environmental concerns over excessive water consumption, drinking water well contamination, and surface water contamination from both drilling activities and fracturing fluid disposal.” In the Marcellus shale region, for example, the Delaware River Basin Commission, responsible for a watershed that serves more than 10 million people, has identified three major areas of concern: reduction of stream flow, pollution of ground and surface water and proper disposal of “frac water.”

• New regulations. These regulations emerging from environmental concerns could significantly impact production and price. IHS Global Insight estimates that simply subjecting hydraulic fracturing to the federal underground injections control requirements in the Safe Drinking Water Act would result in a 20 percent reduction in the number of new wells drilled and a 10 percent loss of natural gas production.

• Cost and sustainability. The eventual cost and sustainability of shale gas production are open to question. Geologist Arthur Berman has argued that the high decline rates will make shale gas wells far more costly than projected, and the current rush to shale gas is a “speculative bubble.” Dow Chemical Co. echoed these concerns in 2009 testimony before the U.S. Senate on the role of natural gas. “Although increased supply from shale gas appears to have changed the production profile, we have seen similar scenarios occur,” Dow testified. “In each case, the initial hopes were too high and production increases were not as large as initially expected.”

America has Bet the House on a big shale gas boom over the next decade (and to a limited extent, LNG imports—see Clemente's testimony). Tomorrow I will focus on the cost and sustainability issues that lie at the heart of the current debate on shale gas production.

03/29/2010

Shale Gas Shenanigans

In the years leading up to the crash of the Housing Bubble in 2006 and the subsequent financial meltdown in 2008, there was no shortage of people telling us America's continued prosperity was not in jeopardy. All that talk was nonsense, of course. In 2010, the situation is eerily similar in the natural gas business. We are told that we have 100 years of supply, implying that we will still be producing cheap shale gas long after the oceans are devoid of fish. As in the pre-Housing Bubble days, a few skeptics are crying foul. There are underground rumblings that things are not on the up & up with shale gas.

The first bone of contention is what the actual production costs are. The Financial Times' John Dizard has been questioning the accepted wisdom lately—

A couple of weeks ago, I quoted Ben Dell, an analyst with Bernstein Research in New York, as estimating the shale gas industry really needs a price of $7.50 to $8 [per mcf] to break even on its all-in costs of finding and producing the stuff, which would be a 60 per cent price rise [over about $5 per mcf]. Not easy for many people, or industries, to pay these days...

So I worked people in the energy service industry, and gas producers to try and refute Ben Dell’s numbers. I couldn’t. My industry sources’ numbers all converged close to $8 per mcf. They do not believe the producers are covering their all-in costs.

For example, as a Texan gas man described the now-hot Marcellus gas fields in Pennsylvania: “One company was saying they can develop reserves there for a little over $1.15 per mcf. If you ask them, they say it costs them $3m to drill and complete wells that average 3bn cu ft of reserves, produced over 40 years. Those reserves are calculated on the basis of high initial production [IP] rates that decline rapidly. There is insufficient data to have an accurate estimate for the assumed life of the wells [for the EUR]. You can’t check any of this, because unlike elsewhere in the US, the state doesn’t release official monthly production numbers for three years”.

“There is a ton of sleight of hand going on here,” he alleges. “The ‘costs’ don’t include the cost of the land, the seismic survey, the operating costs, and other expenses.” Remember, though, that no one with a competent securities lawyer ever needs to tell a lie.

[My note: mcf stands for thousand cubic feet, the standard industry unit of production.]

There are two different magic tricks going on here. First, some costs, like those for the land, are simply left out of the accounting equation. Moreover, shale gas operators like Chesapeake quote very high IP rates on their best wells and estimate a very large ultimately recoverable (EUR) from these wells, despite the fact that decline rates on shale gas wells are typically very steep after the first few months of production. The larger your assumed recoverable per well is, the more profitable your well appears to be. Dizard refers to all this as a sleight of hand, and that's exactly what it appears to be.

Operator production cost estimates look like a form of fraud, but it's the financial and reserves accounting part of things where the stench gets really bad. Here I turn to Allen Brooks' Gas shales: Energy market solution or problem?

Energy investors have embraced the gas shale phenomenon. In fact, if producers don’t have gas shale acreage to highlight in investor presentations — suggesting reserve and production growth — they are ignored in the marketplace. By overstating producing gas shale reserves, companies are able to show extremely favorable finding and development (F&D) economics. Low F&D costs are critical for producers to tap Wall Street for the funds necessary to sustain their aggressive gas shale drilling efforts.

The cost of leases and their relatively short lives have placed a premium on accelerated exploitation. As a result, the industry has been outrunning its ability and desire to complete wells given low natural gas prices. Producers with significant gas volumes previously could hedge at higher prices. This price disparity augmented cash flows. Additionally, large gas shale producers tapped Wall Street for additional capital, entered into joint ventures with larger companies lacking a presence in these plays, and sold assets. But the surge in gas shale production, coupled with the recession and a lackluster demand for natural gas, has pressured gas prices. Producers are now struggling to show both production growth and profitability.

Producers can not demonstrate production growth and profitability in the current low price environment. At the same time, by overstating reserves (EURs) in their shale gas acreage, they can "tap Wall Street" to keep the party going. But wait, it gets worse. Kurt Cobb interviewed B. J. Doyle, vice president of operations for a small Houston-based oil and natural gas exploration company. Here's the clincher—

[Shale gas operators] will drill prospects that they believe have no reasonable chance of doing anything other than breaking even. Why will they do this? To boost stated reserves, a number by which Wall Street judges the value of oil and gas companies.They won't, however, make any true profit on these wells. But they will become what Wall Street calls an "asset play." They will be valued on their assets, in this case stated reserves, rather than on their profitability.

These shale gas producers are an asset play. And this outcome obviously benefits the Wall Street banks who lend them money. Indeed, this is their exit strategy from the unprofitable drilling treadmill they are currently on. If shale gas production can be said to be in a bubble, this is where that bubble lies. And the strategy is working! Rigzone reports on the acquisition frenzy—

BP PLC is expected to announce Tuesday an expansion of its U.S. shale-gas operations through a joint-venture deal in Texas with privately held Lewis Energy Group worth at least $160 million...

BP's move is the latest in a string of deals that have brought major oil companies into U.S. shale gas--a substantial resource that has boosted U.S. gas reserves significantly and is transforming the energy industry... BP, Norway's Statoil SA (STO) and other big oil companies also aim to apply expertise gained in North America to their efforts overseas to extract gas from deep, hard, shale-rock formations.

Several companies have been jostling for acquisitions in the sector, which was pioneered by smaller, independent U.S. producers such as Chesapeake Energy Corp. (CHK) and XTO Energy Inc. (XTO). France's Total SA (TOT) agreed in January to acquire a quarter of Chesapeake's Barnett Shale operations in Texas for $2.25 billion. This came the month after Exxon Mobil Corp. (XOM) gave shale-gas development a definitive stamp of approval by agreeing to acquire XTO in an all-share deal valued at around $31 billion.

What is the upshot of these Shale Gas Shenanigans? As the major oil & gas companies get more involved, the shale gas boom will likely go bust in 2010 and thereafter until prices rise above costs to make production profitable. As Brooks put it, Exxon Mobil "has the financial strength to withstand a low gas price environment and marginal returns from gas shale activity until technology helps to lower development costs." Dizard was simply sarcastic:

The majors, which can’t seem to explore their way out of a grocery bag these days, at least in the onshore US, needed those elastic “reserves” to replace politically risky hydrocarbons in geologically better locations. They, and the remaining independent producers, will be bailed out by gas at $10 an mcf – double today’s level – or higher. Then the service industry will be able to raise prices to cover its full costs.

Don’t tell the political people. Not that they’d listen.

The shale gas boom has been the sole bright spot in America's energy picture, and maybe the only bright spot in the economy as a whole. And what does that bright spot turn out to be? An asset play whereby shale gas producers, conniving with bankers, inflate their own value, hoping to get out while the getting is good.

What else would you expect in 21st century America?

http://kunstler.com/blog/2010/11/sixty-lame-minutes.html

Sixty Lame Minutes

By James Howard Kunstler

on November 15, 2010 9:13 AM

So, last night CBS hauled Aubrey McClendon, CEO of Chesapeake Energy, on board their flagship Sunday infotainment vehicle, 60 Minutes, to blow a mighty wind up America's ass (as they say in professional PR circles). America is lately addicted to lying to itself, and 60 Minutes has become the "go-to" patsy for funneling disinformation into an already hopelessly confused, wishful, delusional, US public.

McClendon told the credulous Leslie Stahl and the huge viewing audience that America "has two Saudi Arabia's of gas." Now, you know immediately that at least half the viewers misconstrued this statement to mean that we have two Saudi Arabia's of gasoline. Translation: don't worry none about driving anywhere you like, or having to get some tiny little pansy-ass hybrid whatchamacallit car to do it in, and especially don't pay no attention to them "green" sumbitches on the sidelines trying to sell you some kind of peak oil story.... It also prepared the public to support whatever Mr. McClendon's company wants to do, because he says his company will free America from its slavery to OPEC. By the way, CBS never clarified these parts of the story by the end of the show.

First of all, they are talking about methane gas, not liquid gasoline or oil. There are large deposits of methane gas locked into shale deposits roughly following the Appalachian mountain chain from New York State through Pennsylvania, West Virginia, into Ohio, but also hot spots out west. It's hard to get at. You have to basically blow up the shale rock deep underground with high pressure water that is loaded up with chemicals and sand particles to keep the rock fragments separated once they are blown apart. Chesapeake Energy specializes in this rock fracturing (or "fracking") method for drilling. You can get gas out of the ground this way. The question is how much, over what time period, at what cost.

At the present time, with America anxious about any kind of future energy, shale gas sounds like a dream-come-true. Mostly what the public saw on 60 Minutes last night was a sell-job for Chesapeake Energy to boost its stock price. Here are some facts:

- Over a 50 year period ahead, all the shale gas drilling of the Marcellus fields in New York State will produce the equivalent of three years US consumption at 2008 levels.

- A price of $8 per unit is required to make shale gas fracking economically viable in theory even for a short time. Gas is currently around $4. Expect to pay at least twice as much for gas.

- Even at higher costs, shale gas fracking is arguably uneconomical. It requires huge numbers of rigs, generally 8 wells per "pad," meaning very high capital investments. The wells produce nicely for a year, average, and then deplete very steeply - meaning you get a lot of money up front and very soon all that capital investment is a wash. Translation: Chesapeake can make a lot quick money over the next few years of intense drilling and they don't care what happens after that.

- Chesapeake itself estimates that 5.5 million gallons of fresh water are needed per well, often delivered in trucks, which require fuel.

- It takes three years, average to prepare a drilling "pad" and the up to 12 wells on it, working 24/7 in rural areas with significant noise and electric lighting

- The fracking fluid is a secret proprietary cocktail formula amounting to 5 percent of the liquid injected into the earth. It's composed of: sand; a jelling agent to suspend the sand because water is not "thick" enough; biocides to kill bacteria that thrive in jelling agent; "breakers" to thin out jell-thickened water after fracking to get the fluid out of the way of released gas and improve "flowback;" fluid-loss additives to decrease "leak-off" of fracking fluid into rock; anti-corrosives to protect metal in wells; and friction reducers to promote high pressures and high flow rates. Of the 5.5 million gallons of fluid injected into each well, 27,500 gallons is the chemical cocktail.

- Mr. McClendon said on 60 Minutes that it couldn't possibly harm the public's water supply because they were drilling so far below the 1000-foot-deep maximum of most water wells. He left out the fact that they have to drill through those drinking water layers to get down to the shale gas, and pump the fracking fluid through it, and then get the gas up through it. He also left out the fact that the concrete casings of drill holes sometimes crack and leak at any depth.

- The fracking fluid cannot be re-used. You have to mix new cocktail fluid for each injection.

- "Flowback" fluid inevitably comes back up with the gas, sometimes spilling over the ground. In any case, the stuff that does come back up is stored on the surface in lagoons. Often it contains heavy metals, salts, and radioactive material from drilling through strata of radon-bearing granite and other layers. Liners of flowback fluid lagoons have been known to fail.

- Gas well failures in Pennsylvania, where production was ramped up quickest in recent years, have ended up polluting well water to the degree that residents can no longer use their wells.

- Little is known about the migration of fracking fluids underground.

It seems to me that the chief mass delusion associated with this touted "bonanza" is that Americans would supposedly be able to shift to driving cars that run on natural gas. I believe they will be hugely disappointed. Between the cost of fracking production (and its poor economics), gearing up the manufacture of a new type universal car engine, and installing the infrastructure for methane gas fill-ups - not to mention the supply operation by either new pipelines or trucks carrying liquefied methane gas, we will discover that a.) America lacks the capital, and b.) that households will be too broke to change out the entire US car fleet.

What this disgusting episode really shows is how eager the USA is to mount a campaign to sustain the unsustainable at all costs, including massive collective self-deception. The lying starts at the very top, not just in Aubrey McClendon's office at Chespeake, but in every executive suite throughout the land - including the Oval Office - where any lie is automatically swallowed and then upchucked for public consumption in the interest of keeping a nation based on addictive rackets stumbling on without having to change our behavior.

from ASPO USA's Peak Oil Review, January 3, 2010

Association for the Study of Peak Oil and Gas - USA

www.aspo-usa.org

Shale Gas: Panacea or Chimera?

The hype surrounding shale gas continued to build during 2010 with many saying that the gas will prove to be so plentiful that it will be the solution to our energy problems for many decades ahead. It has become conventional wisdom in many circles that the US has 100 years’ worth of shale gas ready for exploitation. The hysteria reached its zenith in March at the Cambridge Energy Research Associates annual conference where speaker after speaker spoke ecstatically about the prospects for the natural-gas industry. In Pennsylvania over 1000 shale gas wells have now been drilled. Even India, China, the French and Shell have started investing in the US shale gas bonanza as have the major US oil companies.

During the past year the prices for natural gas fell from $6 per million cubic feet to less than $4 as the quantity of gas in storage continued to build. Outside analysts continue to say that at these prices the industry is losing money and that it will require at least $6 or $7 gas to pay for the drilling and hydraulic fracturing of the expensive horizontal wells.

Concerns over contamination of groundwater by the fracking process continue to grow. Over strident industry objections, the state of New York has put a temporary hold on new shale-gas drilling permits until the EPA can investigate the dangers to groundwater supplies more carefully.

As was the case last year, skeptics point out that while shale-gas wells can initially be very productive they quickly fall to below economic levels. The 100 years’ worth figure comes from the most optimistic possible reading of the Potential Gas Committee report; in reality the amount of gas available at modest prices may ultimately be only a fraction of the touted amount. When one factors in the talk about moving a substantial portion of US electricity generation to natural gas or perhaps replacing the diesels in long-haul trucking with natural gas engines, exponential growth kicks in so that natural gas reserves would be drawn-down much more quickly than imagined.

While large quantities of shale gas are likely to be produced over the next few decades, behind-the- scenes evidence that the resource is not a long-term solution to our energy problems and certainly not to our liquid-fuels problem continues to mount.

getting a little closer to the truth ...

U.S. Cuts Estimate for Marcellus Shale Gas Reserves by 66%

By Christine Buurma - Jan 23, 2012 9:04 AM PT

The U.S. Energy Department cut its estimate for natural gas reserves in the Marcellus shale formation by 66 percent, citing improved data on drilling and production.

About 141 trillion cubic feet of gas can be recovered from the Marcellus shale using current technology, down from the previous estimate of 410 trillion, the department said today in its Annual Energy Outlook. About 482 trillion cubic feet can be produced from shale basins across the U.S., down 42 percent from 827 trillion in last year's outlook.

"Drilling in the Marcellus accelerated rapidly in 2010 and 2011, so that there is far more information available today than a year ago," the department said. The estimates represent unproved technically recoverable gas. The daily rate of Marcellus production doubled during 2011.

The estimated Marcellus reserves would meet U.S. gas demand for about six years, using 2010 consumption data, according to the Energy Department, down from 17 years in the previous outlook.

The Marcellus Shale is a rock formation stretching across the U.S. Northeast, including Pennsylvania and New York. Shale producers use a technique known as hydraulic fracturing, which involves pumping water, sand and chemicals underground to extract gas embedded in the rock.

Geological Data

The U.S. Geological Survey said in August that it would reduce its estimate of undiscovered Marcellus Shale natural gas by as much as 80 percent after an updated assessment by government geologists.

Shale gas will probably account for 49 percent of total U.S. dry gas production in 2035, up from 23 percent in 2010, the Energy Department said today.

Gas's share of electric power generation will increase to 27 percent in 2035 from 24 percent in 2010, the report showed.

The department also said the U.S. may become a net exporter of liquefied natural gas in 2016 and a net exporter of natural gas in 2021. U.S. LNG exports may start with a capacity of 1.1 billion cubic feet a day in 2016 and increase by an additional 1.1 billion cubic feet per day in 2019, the department said.